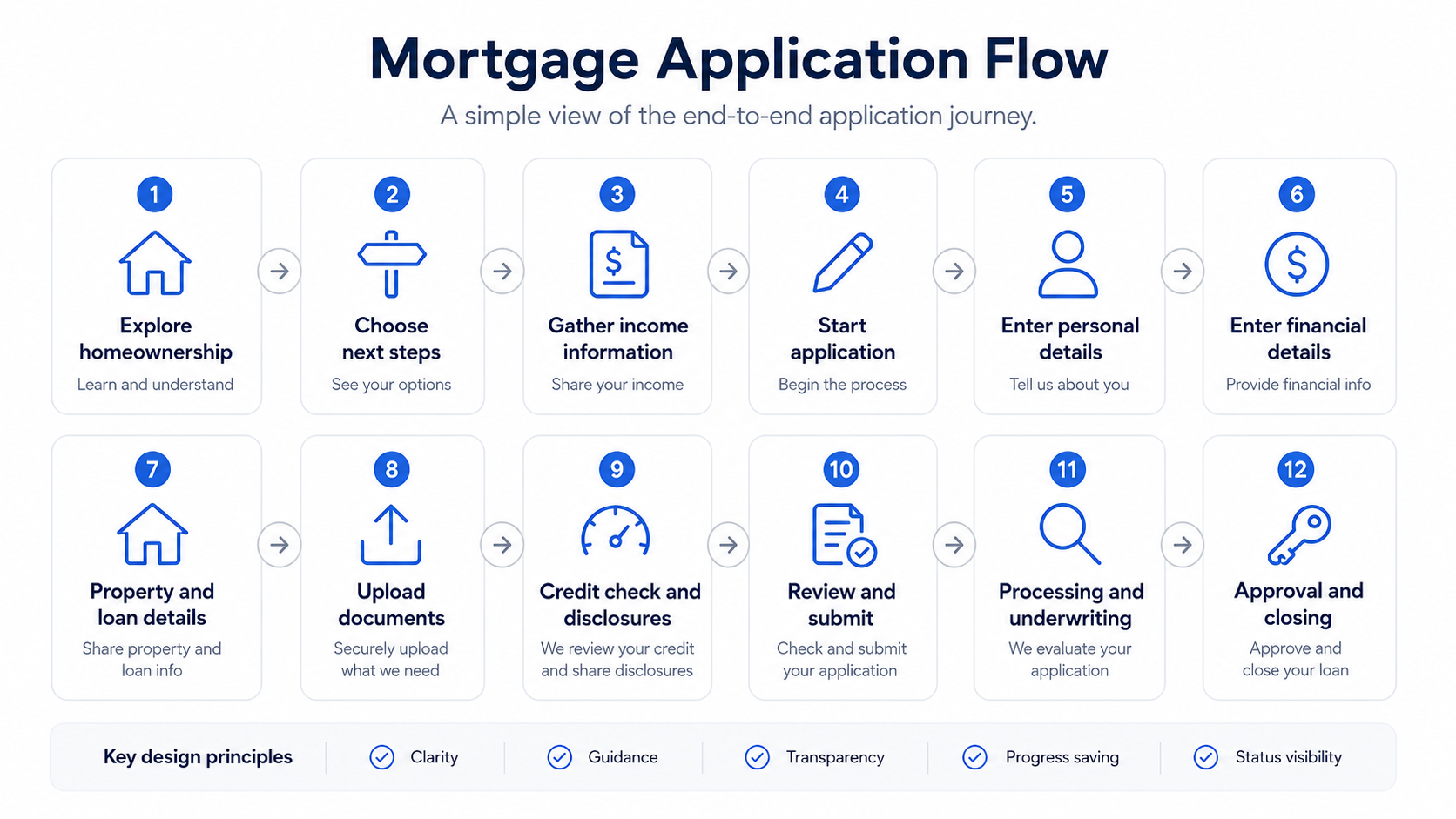

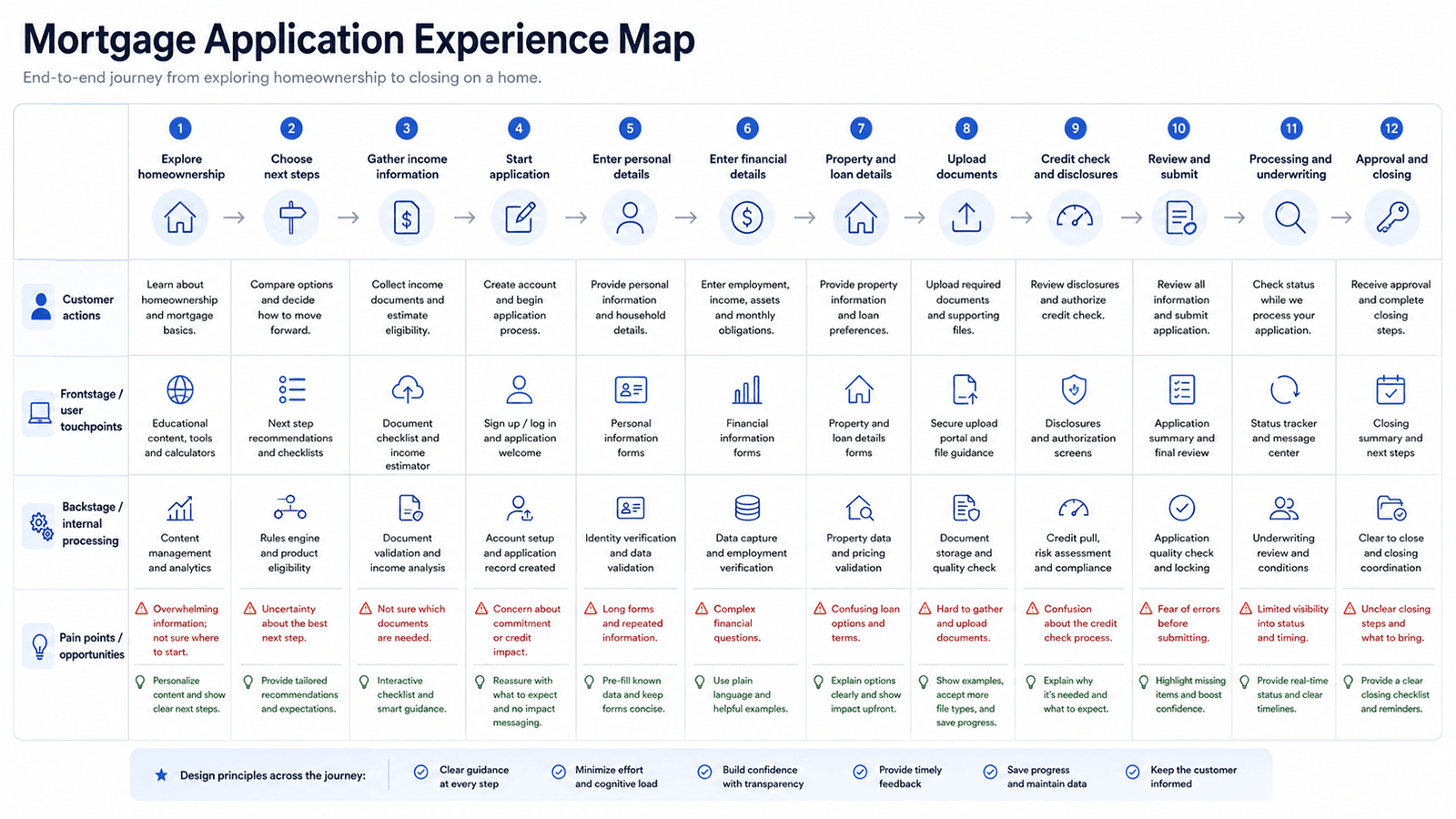

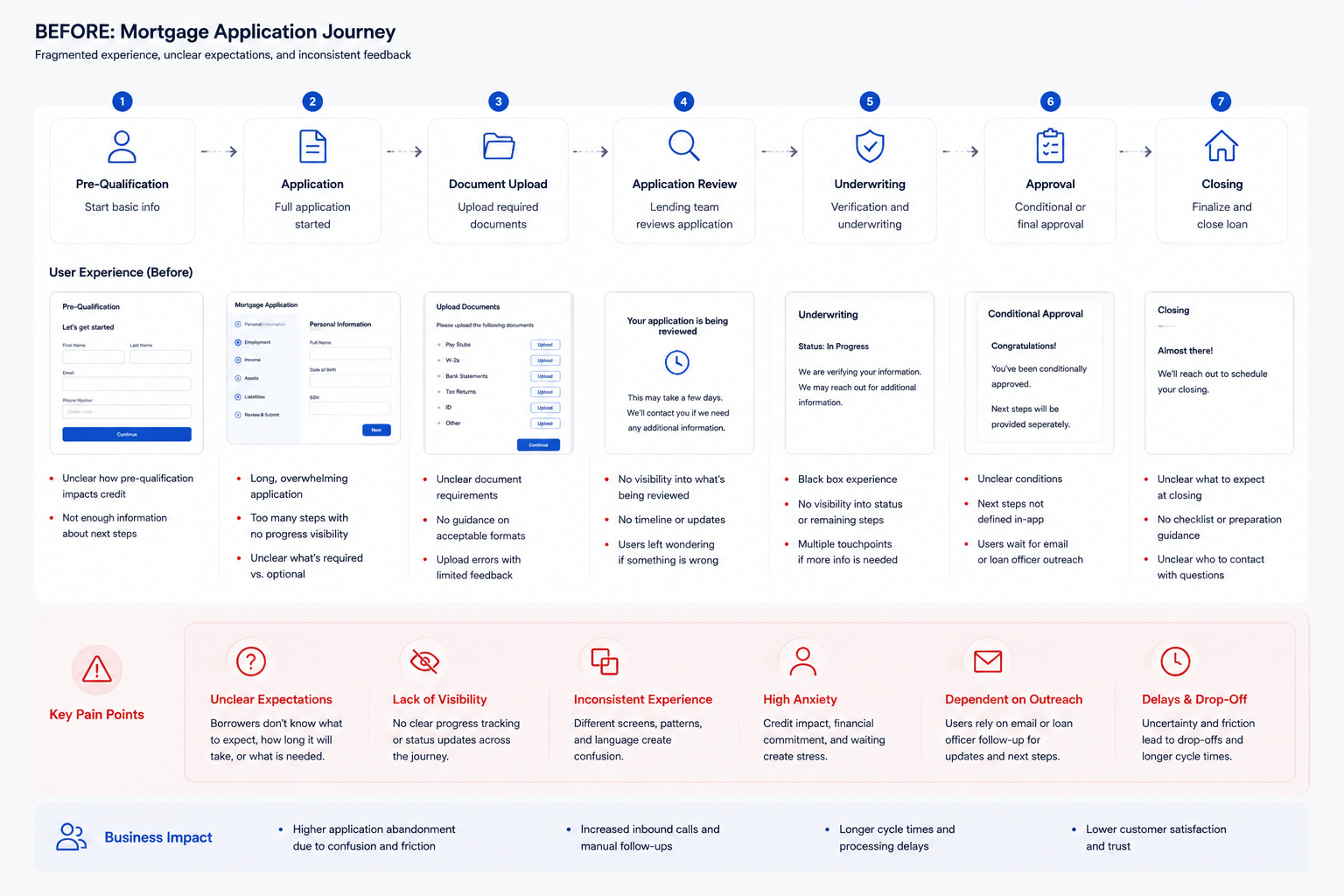

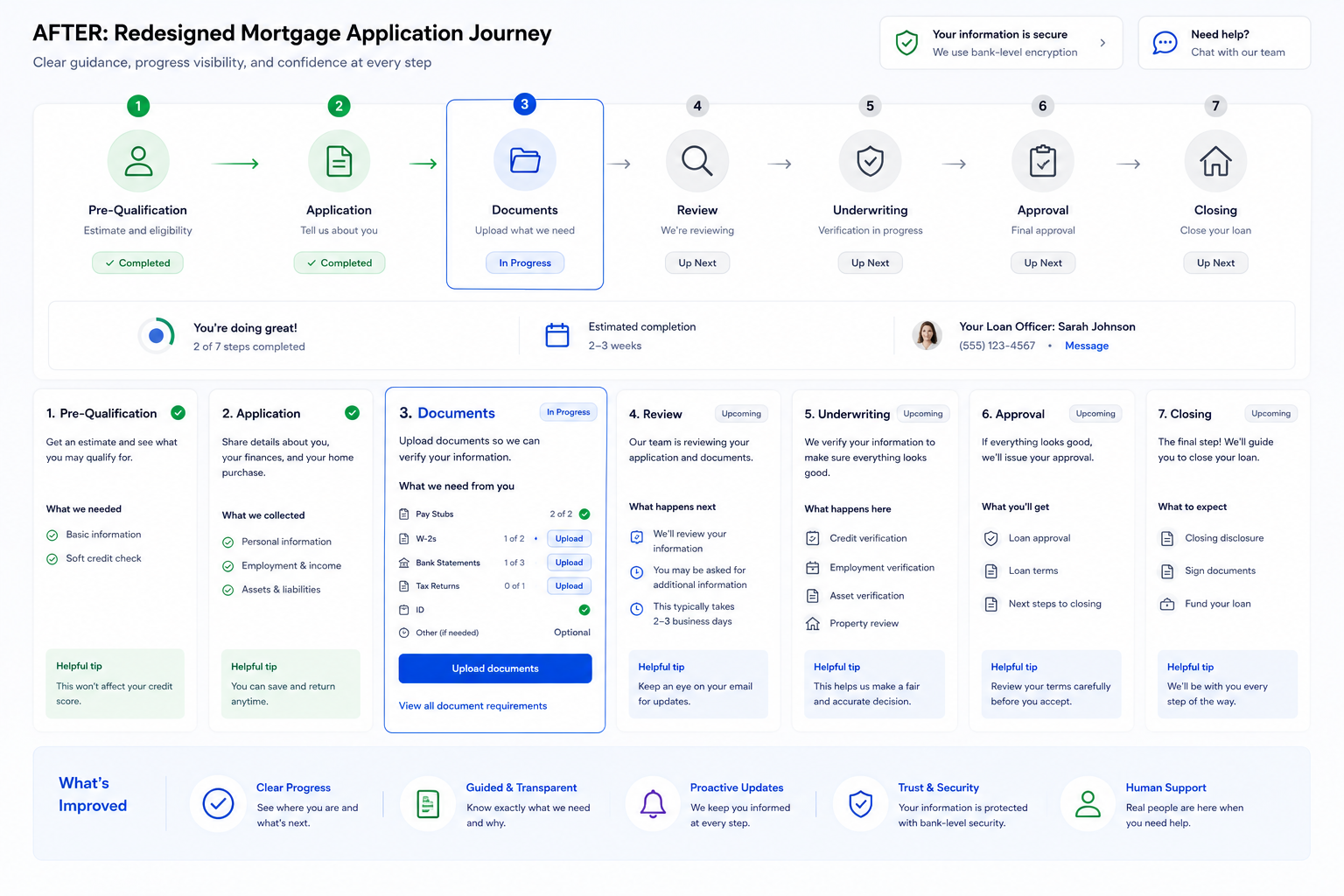

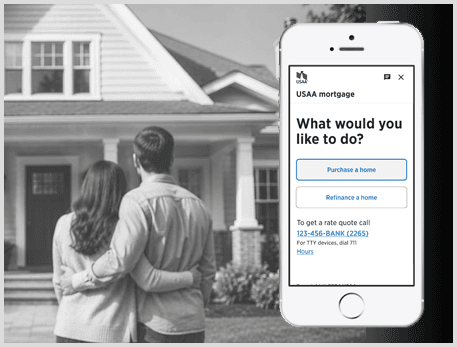

Project Summary

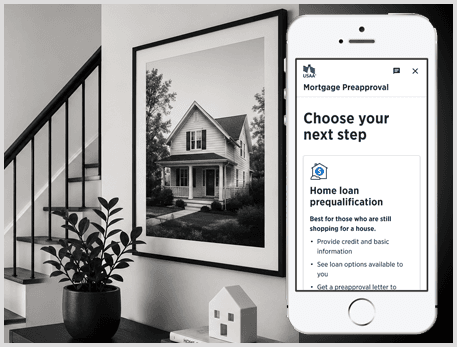

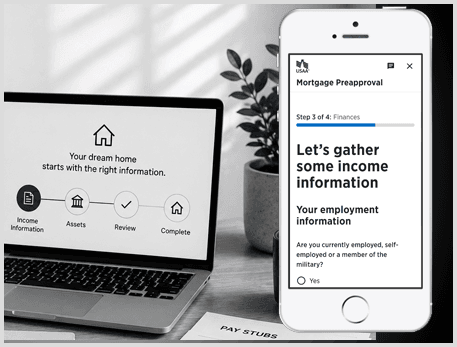

The mortgage application journey was a sensitive, high-consideration financial workflow designed for borrowers applying for a mortgage online. These users were making a major financial decision and had to move through multiple steps, provide personal and financial information, understand credit-related requirements, gather documents, and wait for system or lending team feedback. Many borrowers were unfamiliar with the mortgage process, so moments involving credit checks, document requirements, and unclear next steps created hesitation and uncertainty.

My focus was to make the experience clearer, more guided, and easier to complete by improving progress visibility, reassurance, and next-step guidance without removing required steps, weakening compliance expectations, or oversimplifying important lending decisions.